When Procurement Became Anti-Procurement: How European Defence Acquisition Inverted Its Own Function, 1945–2026

Procurement, in 1945, was the function that delivered military capability to the armed forces. By 2026, in the European Union and across its Member States, it had become the function that prevented that delivery. The instruments (Directive 2009/81/EC Article 47, TFEU Article 346 practice, Member State implementing legislation, NSPA International Competitive Bidding) operate as designed. The design is the inversion. A companion analysis to ISC’s 11 May 2026 study of the parallel United States case.

Key Acronyms (used throughout)

At a Glance

- Thesis. Procurement, as exercised in European defence acquisition in 2026, no longer performs the function the word originally named. It performs its opposite. The rule layer (Directive 2009/81/EC, Member State implementing legislation, TFEU Article 346 practice, NSPA “L1” lowest-compliant selection) selects against the capability outcomes the rule was meant to deliver.

- Periodisation. Four waves of inversion: 1957 Sandys Defence White Paper; 1971 GIAT corporatisation; 1987 Royal Ordnance sale to British Aerospace; 2009 European Union Directive 2009/81/EC.

- Mechanism. A five-step inversion chain converts rule into structure: rule writes price above resilience; contractor optimises to single facility; consolidation cascades; strategic-input nodes collapse to single or near-single sources; the procurement notice itself publishes the chokepoint map.

- Energetics duopoly. Eurenco (France/Sweden/Belgium, formed 2004 from SNPE Matériaux Énergétiques + NEXPLO Industrier AB / Bofors Explosives + PB Clermont) and the parallel Nitrochemie joint venture (Rheinmetall–RUAG, formed 1998, plants at Wimmis (CH) and Aschau am Inn (DE)) together constitute the Continental European energetics layer. Both are single-line-of-failure at site level for military-grade hexogen (RDX), octogen (HMX), nitroguanidine and the NTO/FOX-7 precursor chain feeding STANAG 4439 / AOP-39 IM-compliant fills.

- Empirical verdict. The Ukraine 155 mm demand signal of 2022–2026. The European Union one-million-round target for the year to March 2025 was missed; cumulative deliveries through that window assessed in a range of approximately 450,000–600,000 rounds. Aggregate capacity has since risen substantially, with Member State and Commission projections of 1.7–2.0 million rounds per year by end-2026, while the structural condition that produced the original shortfall has not been resolved at the rule layer.

- Restoration path. Reversing the inversion is a rule-layer task. Directive 2009/81/EC Article 47 amendment; mandatory STANAG 4170 / AOP-7 dual-qualification for HD 1.1 strategic energetics; STANAG 4107 / AQAP-2110 surge-clause enforcement; Union-level Strategic Energetics Reserve. None of these is delivered by ASAP, EDIP or ReArm Europe, which operate at the appropriation layer.

On 11 May 2026, ISC Defence Intelligence published two companion analyses on the United States precision-munitions industrial base. The first [1] argued that the visible failure of the United States arsenal during the March 2026 Iran War was not a failure of investment or a failure of strategic foresight. It was what one specific procurement mechanism reliably produces: source-selection on a defence contract on the basis of the lowest technically compliant bid. The second analysis [2] deepened that argument into a Research and Analysis, Defence (RAND)-style report with full source tiering, periodisation and a five-step pathology chain.

Both pieces were anchored in the United States. They referenced European institutions tangentially and deliberately. This companion analysis inverts the frame, geographically and conceptually.

The geographic inversion is straightforward: the European Union, the United Kingdom and the European Free Trade Association (EFTA) economies adjacent to the Union ran the same experiment, in different statutes, on a roughly parallel timeline, and arrived at structurally the same result. That story is told in Sections 1 to 6 below.

The conceptual inversion is the sharper claim, and it sits in the title of this piece. Procurement, as the word was understood in the European defence ministries of the immediate post-war period, named a specific function: the function of obtaining for the armed forces, at the time required, in the quantity required, at the quality required, the materiel necessary for them to perform their assigned military tasks. That function had built-in obligations to industrial-base resilience, to surge capacity, to dual qualification and to strategic reserve, because the Second World War had just demonstrated, at the cost of tens of millions of European lives, what happens when those obligations are not honoured.

By 2026, in the European Union and across its principal Member States, the function had inverted. The activity still bears the name procurement. The instruments still call themselves procurement instruments. The officials still hold procurement titles. But the activity those officials perform, constrained by the rule layer they are required to follow, produces an outcome that is the opposite of what the original function was meant to produce. Lowest-price selection at the strategic-input layer produces single-point-of-failure industrial concentration. National-champion ringfencing under TFEU Article 346 produces consolidated, fragile primes. Process-compliance discipline produces decision latencies that exceed the response times required by the operational environment. A procurement system that cannot, under demand, procure the items it exists to procure is not performing the function it names. It is performing the function’s inverse.

This piece names that inversion. It traces when it happened, by what rule, under what political authority. And it asks what restoring procurement, understood as the original function, would now require.

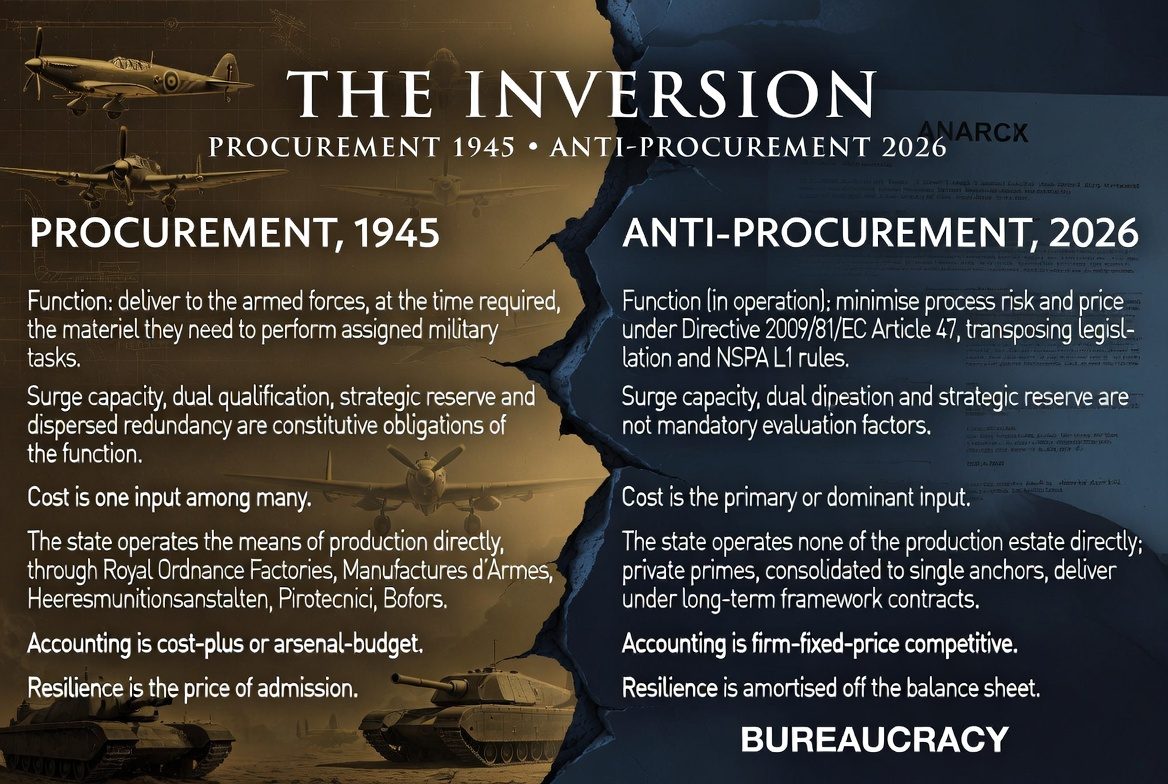

The Inversion, in Two Columns

1. The European Arsenal of 1945: Procurement Working as Designed

The European Allied arsenal of the Second World War, like the American one, was a deliberately redundant mesh. It was distributed by national policy, not by accident or by market outcome. Five strands ran through it.

1.1 The United Kingdom: ROFs, RNADs and the Commonwealth Production Chain

The Royal Ordnance Factory (ROF) estate at peak operated forty-two production sites across the United Kingdom [1]. These ranged from filling stations (ROF Bridgwater, ROF Glascoed, ROF Chorley, ROF Risley, ROF Aycliffe, ROF Ranskill, ROF Pembrey, ROF Bishopton, ROF Powfoot, ROF Drigg) through propellant and small-arms ammunition factories at Radway Green and Birtley to specialist heavy-calibre, fuze, projectile and explosive-fill capacity. Each was state-owned, state-operated, and run by the Royal Ordnance Factories Directorate within the Ministry of Supply. The estate was, in the strict sense of the word, the means of production of the United Kingdom’s ammunition. The Crown owned it. The Crown ran it.

Parallel to the production estate the Royal Naval Armament Depots (RNADs) maintained the Royal Navy’s ordnance and explosives across a separate network of storage, assembly and outload facilities. The principal RNAD sites of the wartime and immediate post-war period included Priddy’s Hard (Gosport), Bedenham (Gosport), Bull Point (Devonport), Ernesettle (Plymouth), Frater (Gosport), Crombie (Rosyth), Beith (Ayrshire), Coulport (Argyll, later the dedicated Royal Navy strategic weapons depot), Glen Douglas (the NATO Forward Munitions Depot for the Eastern Atlantic, opened 1968), Trecwn (Pembrokeshire), Dean Hill (Wiltshire) and Broughton Moor (Cumbria) [2]. The RNAD network was the Royal Navy’s strategic ammunition reserve. It was operated by the Admiralty, then by the Ministry of Defence (Navy), under the same direct-state-control logic as the ROF estate.

Beyond the United Kingdom the Commonwealth chain extended through Canadian Industries Limited’s Defence Industries Limited (DIL) plants, Cherrier, Pickering, Saint-Paul-l’Ermite, Verchères, Nobel, Valleyfield, Bowmanville, and Australian and New Zealand small-arms ammunition factories at Footscray, Hendon, Welshpool and Mount Wellington. The Commonwealth surge architecture of 1944–1945 was as deliberately distributed as the American Government-Owned, Contractor-Operated (GOCO) mesh, and for the same reasons.

1.2 France: The Manufactures d’Armes and the SNPE Energetics Spine

France entered 1945 with a state arsenal system already in administrative reset following the Vichy interlude. The pre-war Manufactures d’Armes Nationales at Saint-Étienne (MAS), Tulle (MAT), Châtellerault (MAC) and Bayonne (MAB) were reconstituted under the Service Technique de l’Armement, and the explosives and propellants estate was reorganised under the Service des Poudres into what would become, in 1971, the Société Nationale des Poudres et Explosifs (SNPE). The Atelier de Construction de Bourges (ABS), Atelier de Construction de Tarbes (ATS), Atelier de Construction de Roanne (ARE) and Atelier de Construction de Puteaux (APX) anchored the heavy-weapon and armoured-vehicle construction estate. The energetics spine ran through Bergerac, Pont-de-Buis, Sorgues, Saint-Médard-en-Jalles and Vert-le-Petit. The arsenal model was unambiguously sovereign, redundant by design and operated under cost-plus accounting through the délégation ministérielle pour l’armement (the predecessor of the DGA, established 1961).

1.3 Germany: The Heeresmunitionsanstalten Legacy and the Bundeswehr Reset

The German wartime ammunition estate, the network of Heeresmunitionsanstalten (HMA, generally abbreviated Muna), was dismantled by Allied control after 1945. Significant sites were destroyed; others were converted to civilian use; a residual estate became the basis of the West German federal munitions reserve when the Bundeswehr was established in 1955. From the late 1950s the post-war German defence industrial base reformed around private actors: Rheinmetall (re-founded 1956), Diehl, Heckler & Koch (founded 1949 by former Mauser engineers), Mauser-Werke Oberndorf, Junghans, Dynamit Nobel (the legacy explosives concern), Buck-Werke and a constellation of medium-calibre, fuze, propellant and pyrotechnic specialists. East German production was reorganised under Volkseigene Betriebe (VEB) state combines and disappeared as a separate entity in 1990–1991.

1.4 Italy: BPD, Pirotecnici and the State Holding Model

The Italian state arsenal estate of 1945 included the Pirotecnico di Capua and Pirotecnico di Bologna, the Fabbrica d’Armi di Terni and the Bombrini Parodi-Delfino (BPD) energetics complex at Colleferro. After 1945 the estate was reorganised through the state holding system, principally Istituto per la Ricostruzione Industriale (IRI) and Ente Nazionale Idrocarburi (ENI), with Finmeccanica (founded as an IRI engineering holding in 1948) consolidating the senior defence portfolio. BPD became the energetics anchor; SNIA-BPD, later SNIA Difesa Spazio and ultimately Avio, spun off propulsion and energetics specialities. Beretta, Breda, Oto Melara, Officine Galileo and a long tail of medium-calibre and fuze houses sat alongside.

1.5 The Smaller Producers and the Nordic Spine

The Belgian Fabrique Nationale d’Armes de Guerre (FN Herstal), the Czechoslovak Ćeskoslovenská Zbrojovka (CZ) and the Spanish Empresa Nacional Santa Bárbara, together with smaller national arsenals in the Netherlands (Artillerie Inrichtingen), Denmark (Ammunitionsarsenalet Frederikshavn) and Norway (Råufoss Ammunisjonsfabrikker), rounded out the Continental Western European production estate. To the north, the Swedish AB Bofors at Karlskoga was the senior single-firm anchor for medium-calibre, naval gun, anti-aircraft, propellant and energetics work, with the FFV (Försvarets Fabriksverk) state arsenal estate covering the smaller-arms tail.

In its 1945–1955 form, the European arsenal mesh was, taken together, comparable in scale to the United States GOCO estate and substantially more diverse politically. Each nation operated its own production system, by national policy, under cost-plus or arsenal-budget accounting, with surge capacity treated as a national insurance obligation rather than a programme line item. The mesh was the architecture. Procurement, in 1945, was working as designed.

2. The Long Inversion, 1957–2009: Four Waves

The inversion did not arrive as a single event. It came in four overlapping waves, each driven by a different rule shift. The first three preceded the European Union procurement framework of 2009; the fourth is the framework itself.

2.1 Wave One — The Sandys Reset and the British Reorganisation, 1957–1973

The 1957 United Kingdom Defence White Paper of Duncan Sandys was, in retrospect, the first major rule-layer shift in the European post-war industrial base [3]. The White Paper’s shift toward strategic nuclear deterrence and reduced conventional standing forces translated, on the industrial side, into a programme of ROF closures and rationalisations through the 1960s. ROF Birtley, ROF Aycliffe, ROF Hereford, ROF Ranskill, ROF Pembrey and ROF Risley all reduced or closed across the 1957–1970 window. The conventional ammunition estate was directed to amortise toward a smaller national requirement. By the late 1960s the ROF estate had contracted from its wartime peak of forty-two sites to a working core of approximately twelve to fifteen production sites, a contraction of roughly two-thirds, achieved by administrative decision, not by any market process.

In parallel the Royal Naval Armament Depot estate was rationalised. RNAD Trecwn was wound down (formally closed 1993). RNAD Dean Hill closed (2004). RNAD Broughton Moor went out of service. Bull Point, Ernesettle and Bedenham were progressively consolidated. The Eastern Atlantic NATO Forward Munitions Depot at Glen Douglas, opened 1968 in response to the Cuban Missile Crisis-era acknowledgement of insufficient forward-deployed Alliance ammunition, became the principal residual deep-magazine site. The Coulport site was redirected, from the late 1960s onward, to the Royal Navy’s strategic weapons system role.

The inversion logic of Wave One was the subordination of capability requirement to budget envelope. The White Paper did not, in its language, abolish the procurement function. It re-prioritised it: a smaller conventional force needed less ammunition, less production capacity, less reserve. The unstated assumption was that the smaller envelope was the new ceiling, not a temporary contraction from which the system could re-expand. Surge capacity, when retained, was retained on paper as a notional standby. The means of operating it, the trained workforce, the warm production lines, the qualified energetics chains, was not retained as a budgetary obligation.

2.2 Wave Two — The French and German Reorganisations, 1971–1989

The French rule-layer shift came in 1971 with the creation of GIAT (Groupement Industriel des Armements Terrestres) as a holding bringing together the Manufactures d’Armes and the Ateliers de Construction under a single industrial-policy structure. GIAT was reconstituted as a société nationale (state company) in 1990 under French parliamentary statute. The reform’s explicit purpose, on the French Government’s own statement of 1990, was to convert the arsenal estate from a cost-plus public-administration model into a competitive industrial actor. The conversion ran into structural difficulty: GIAT’s headcount fell from approximately seventeen thousand to around seven thousand between 1990 and 2005, with multiple cycles of capital recapitalisation by the French Treasury [4]. GIAT was renamed Nexter in 2006, merged with Germany’s Krauss-Maffei Wegmann (KMW) in 2015 to form KMW+Nexter Defense Systems (KNDS); on KNDS Group disclosures for 2024 the combined headcount was reported in the region of nine to ten thousand.

The German rule-layer shift was different in character but parallel in effect. From the 1970s through the late 1980s the Federal Republic of Germany progressively concentrated medium-calibre and propellant work in Rheinmetall and Dynamit Nobel; small-arms work in Heckler & Koch and Mauser; missiles in Bayern-Chemie and the Diehl group; armoured vehicles in Krauss-Maffei, MaK and Henschel (later combined as KMW). The pattern was driven by a combination of Federal Procurement Office (Bundesamt für Wehrtechnik und Beschaffung, predecessor of BAAINBw) cost discipline, by Bundeswehr budget envelopes, and by the steady absorption of secondary firms into the senior houses. The 1989–1991 unification absorbed and then largely dissolved the East German Volkseigene Betriebe defence portfolio.

The inversion logic of Wave Two was corporatisation. The state did not yet withdraw from ownership in France; it withdrew from the operating function. In Germany the function had already been delegated to private actors; the rule-layer change consolidated that delegation. The procurement function, defined in 1945 as direct state control of the means of producing materiel, became in Wave Two the function of contracting with private firms. The state remained the customer. It ceased to be the operator.

2.3 Wave Three — The Royal Ordnance Privatisation and the British Aerospace Consolidation, 1984–1999

The single largest discrete European industrial-base event of the post-war period was the corporatisation of Royal Ordnance in 1984 and its sale to British Aerospace in 1987 [5]. The Royal Ordnance Factories, having already contracted across the 1960s and 1970s, were grouped into Royal Ordnance plc on 2 January 1985 and offered for sale. British Aerospace acquired the company on 22 April 1987 for approximately £190 million, a figure widely characterised at the time, including by the National Audit Office, as low [6]. The acquisition transferred the ROF site portfolio, the explosives and propellants estate, the small-arms ammunition capacity (Radway Green), the heavy-calibre estate (Birtley and Glascoed) and the historic Enfield small-arms designs into private commercial control.

The post-1987 trajectory was rationalisation. ROF Patricroft closed (1988). ROF Bridgwater closed (1990). ROF Chorley closed (2007). ROF Powfoot closed (2010). The Royal Ordnance Defence Systems Group went through a series of internal reorganisations within BAE before the residual operations were rebadged as BAE Systems Land Systems Munitions (later BAE Systems Land UK) and absorbed into the wider BAE Systems plc structure. Today the residual ROF estate operates at four primary sites: Glascoed (filling), Radway Green (small-arms ammunition), Bishopton (propellants, closed and replaced by capacity at Glascoed through the Munitions Acquisition and Supply Solution, MASS, in 2012), and a small specialist tail. From forty-two production sites in 1945 to four in 2026, achieved by privatisation, then by consolidation, then by a single long-term framework contract [7].

The Munitions Acquisition and Supply Solution (MASS) and its successor, NGMS

The United Kingdom’s Munitions Acquisition and Supply Solution (MASS), awarded to BAE Systems Land UK in 2008 for an initial fifteen-year term, was the single-supplier framework through which the Ministry of Defence procured the substantial majority of its domestic ammunition. MASS was succeeded in 2023 by the Next Generation Munitions Solution (NGMS), again anchored on BAE Systems Land UK, on a multi-year extension. Both instruments were treated as falling under the equivalent national security carve-out and were not procured under European Union Directive 2009/81/EC. They illustrate a wider point: the Union rule layer is one input into the European industrial base; national rule layers operating under TFEU Article 346 are another, and in many cases the more determinative one. MASS and NGMS are national rule-layer choices, not Union-level ones. They are the United Kingdom’s long-term, single-supplier, sole-source equivalent of the United States Government-Owned, Contractor-Operated framework.

The inversion logic of Wave Three was the withdrawal of state ownership. Until 1987 the Crown owned the means of production of British ammunition. After 1987 it did not. The procurement function was then defined, in practice, as the function of writing contracts with the new private owner. The Crown’s capability to direct industrial activity in defence of essential security interests, the capability that TFEU Article 346 would later codify as a Member State prerogative, was reduced, in the United Kingdom case, to the capability to contract.

2.4 Wave Four — European Union Directive 2009/81/EC and the Codification of Anti-Procurement

The fourth wave was Union-level. European Union Directive 2009/81/EC, the Defence and Sensitive Security Procurement Directive, was adopted on 13 July 2009 and transposed into Member State law by 21 August 2011 [8]. The Directive established the procedural framework for defence and security contracts above specified value thresholds across the European Union internal market, restricted procedure, negotiated procedure, competitive dialogue and (in narrow circumstances) negotiated procedure without prior publication.

On the source-selection rule, Directive 2009/81/EC Article 47 specified two permitted award criteria: lowest price only or most economically advantageous tender (MEAT). The structural parallel with United States Federal Acquisition Regulation (FAR) 15.101 is exact: the European Member State contracting authority chooses between a strict price-only rule and a multi-criteria rule. The Directive did not mandate consideration of surge capacity, dual qualification, geographic dispersion, or industrial-base resilience as either a permissible technical criterion or a mandatory evaluation factor. Member States were free to write such criteria into specific tenders; they did so unevenly, and not enough overall to alter the consolidation trend.

TFEU Article 346 (originally Article 296 of the Treaty Establishing the European Community), preserved by Directive 2009/81/EC, allows a Member State to derogate from internal market rules where it considers a measure necessary for the protection of essential security interests connected to the production of or trade in arms, munitions and war material. In practice, Member States have used Article 346 to ringfence national champions and protected supply chains, not to mandate surge capacity. The Directive’s rule layer and the Treaty’s escape valve operated in mutually-reinforcing fashion: the Directive set lowest-price or MEAT as the default; the Treaty permitted national-champion ringfencing as the exception. Neither rewarded distributed industrial-base resilience.

The inversion logic of Wave Four was codification. What had been three decades of administrative drift, national ROF closures, GIAT corporatisation, Royal Ordnance privatisation, was, in 2009, written into Union law as the default procedural framework. The procurement official was, after transposition, no longer permitted to make an industrial-base resilience case as the dominant award criterion without active national-level legal cover. The presumption of the Directive ran the other way. After 2011, Continental procurement of defence materiel above threshold became, by Union law, biased in both rule and procedure toward the consolidation outcome the original procurement function was meant to prevent.

3. The Mechanism of Inversion: Five-Step Chain

The original 11 May 2026 special report set out a five-step pathology chain from rule to industrial structure. The same chain operates in Europe, with European-specific terminology, as the mechanism by which procurement becomes anti-procurement.

Step 1, The rule. Directive 2009/81/EC Article 47 permits lowest price or MEAT. National implementing legislation, the United Kingdom’s Defence and Security Public Contracts Regulations 2011 (DSPCR), France’s Code des marchés publics de défense ou de sécurité, Germany’s Vergabeverordnung Verteidigung und Sicherheit (VSVgV) and equivalents, transposed the rule. National practice within MEAT trended toward price-weighted scoring with limited weight on industrial-base factors.

Step 2, The contractor response. Award convergence to lowest qualified bid rewards single-facility, single-line, just-in-time production. European primes responded to the Directive’s incentives in the same direction the American primes responded to FAR 15.101: by minimising standing overhead, by concentrating output in single anchor facilities, by amortising surge capacity off the balance sheet, by treating second-source qualification as a programme-specific cost rather than a strategic insurance.

Step 3, The consolidation cascade. Continental medium- and small-calibre ammunition consolidated into Rheinmetall (through acquisitions of Mauser, RWM Schweiz, Buck, RUAG Ammotec, Vytáhneíce). Energetics consolidated, on one side, into Eurenco (France/Sweden/Belgium, formed 2004 from SNPE Matériaux Énergétiques + NEXPLO Industrier AB / Bofors Explosives + PB Clermont) and, on a separate and parallel track, into the Nitrochemie joint venture (Rheinmetall–RUAG, formed 1998, plants at Wimmis (CH) and Aschau am Inn (DE)). Land systems consolidated into KNDS (Nexter + KMW, 2015), the General Dynamics European Land Systems holding (incorporating Steyr-Daimler-Puch, Mowag and Santa Bárbara Sistemas from 2001 onward), and the BAE Systems Land portfolio. The naval and missile sectors followed parallel paths through Naval Group, Fincantieri, Navantia, MBDA (the Anglo-Franco-Italian missile consolidator formed in 2001) and Saab Dynamics.

Step 4, Single-source nodes at the strategic input layer. Above all in energetics. Military-grade RDX (1,3,5-trinitro-1,3,5-triazinane / hexogen) and HMX (octahydro-1,3,5,7-tetranitro-1,3,5,7-tetrazocine / octogen) are produced at Eurenco Bergerac/Sorgues/Pont-de-Buis and at Nitrochemie Wimmis/Aschau am Inn. Both producers also supply NTO (5-nitro-1,2,4-triazol-3-one) and FOX-7 (1,1-diamino-2,2-dinitroethylene) precursors for the insensitive-munition (IM) plastic-bonded explosive (PBX) fills required for compliance with STANAG 4439 and AOP-39. Loss of either Eurenco or Nitrochemie at site level, through industrial incident, infrastructure failure, regulatory intervention or adversary action, is a Continental capability event. The European energetics layer is, in 2026, an effective duopoly at the strategic-precursor level.

Step 5, The transparency layer. The European Union’s Tenders Electronic Daily (TED) publishes the procurement notices that map the chokepoints. The NATO Support and Procurement Agency (NSPA) eProcurement 5G portal publishes the Alliance-level equivalents. STANAG 4170 / AOP-7 qualification reporting, STANAG 4439 / AOP-39 IM compliance dossiers, and STANAG 4107 / AQAP-2110 quality-assurance documentation are open or semi-open under Union and NATO transparency rules. A motivated adversary can construct the European single-source map from open data more easily than the underlying industrial actors can construct their own collective contingency plan. The transparency that the Directive required, the inversion required for itself.

The chain is the same as the American chain. The instruments are different. The structural result is the same. The function, traced step by step, performs the opposite of what its 1945 definition required.

4. Where the Inversion Has Landed in 2026: The Single-Source Nodes

The European industrial base in 2026 is, at the strategic input layer, characterised by a small number of load-bearing single or near-single-source nodes. The map below is open-source, derived from Member State procurement notices, EU and NATO procurement publications, company disclosures and industrial press reporting. It is not exhaustive. It is sufficient to make the structural point.

| Strategic input | Principal European producer(s) | Secondary / alternative | Mitigation horizon if primary lost [ISC Estimate] |

|---|---|---|---|

| Military-grade RDX / HMX (hexogen / octogen) | Eurenco (Bergerac, Sorgues, Pont-de-Buis, FR); Nitrochemie (Wimmis, CH, Aschau am Inn, DE) | United States Holston Army Ammunition Plant (subject to STANAG 4170 / AOP-7 qualification timeline) | 24–48 months for qualified surge to second European source |

| NTO & FOX-7 precursors for IM PBX fills (STANAG 4439 / AOP-39 compliant) | Eurenco, Nitrochemie | Limited Nordic capacity (Nammo Vihtavuori); United States qualified pathway | 24–48 months |

| Single-/double-/triple-base propellants | Eurenco, Nitrochemie, Nammo (Vihtavuori, FI) | Bofors propellant; small Czech and Polish producers | 12–24 months for cross-qualification |

| 155 mm projectile filling (HE) | Rheinmetall (Niedersachswerfen, Unterlüss); BAE Systems Glascoed (UK); Nexter Bourges (FR); Expal Granada (ES); Czech CSG sites | Nammo Råufoss filling lines; Italy Simmel Difesa; Pearson Engineering | 12–18 months at marginal capacity |

| Medium-calibre ammunition (20–40 mm) | Rheinmetall (DE/CH/IT); Nammo (NO/FI/SE/FR) | FN Herstal; CBC-Magtech | 9–15 months |

| Small-arms ammunition (5.56, 7.62, 9 mm) | Nammo; FN Herstal; RUAG Ammotec; Sellier & Bellot (CSG) | Multiple Eastern European producers | 6–12 months |

| Seeker assemblies (IR / radar / dual) | MBDA; Diehl Defence; Thales | Saab Dynamics; limited Israeli / United States options | 18–36 months for new sub-tier qualification |

| Solid rocket motors (large) | Avio (IT); Bayern-Chemie (DE, MBDA); Nammo Raufoss / Nammo Belin (FR) | Roxel (FR/UK MBDA joint venture) | 18–36 months |

| Tank gun forging (120 mm L/55 smooth-bore) | Rheinmetall Waffe Munition (Unterlüss / Bergen-Belsen, DE) | None at EU/EEA scale as of May 2026. Mitigation requires BAE Systems Land UK (post-Brexit, non-EU but Allied) or United States Watervliet Arsenal qualification pathway. | 36+ months for new qualified producer at scale |

| Rare-earth refining and permanent magnets (NdFeB) | None at military-grade industrial scale in EU 2026 | External (principally China; some Australia, Estonia, Vietnam emerging) | Indefinite at current production architecture |

| Mitigation horizon column — ISC analytical estimate, not citation-anchored. Horizons reflect ISC’s assessment of qualified-source recovery times under typical STANAG 4170 / AOP-7 qualification cycles and observed industry lead times. Specific recovery times for any individual node may differ; figures are indicative. 2027 aggregate-capacity note. Per Commission, Member State and industry projections through March–April 2026, European new-build 155 mm capacity is projected in the range of approximately 1.5 to 2.0 million rounds per year by end-2026, with the Rheinmetall Niedersachswerfen line projected on Rheinmetall public communications at a rate in the several-hundred-thousand-rounds-per-year band once fully ramped, and incremental capacity from BAE Glascoed, Nexter Bourges, Expal Granada and CSG sites contributing the balance. The aggregate-capacity figure does not itself resolve the single-source dependency at the upstream energetics, propellant and tank-gun-forging layers, which remain the binding constraints under high-intensity-conflict demand profiles. | |||

The pattern is the American pattern translated into European institutions. Where the United States precision-munitions architecture has single-source nodes at Holston (RDX/HMX), Radford (propellants), McAlester (filling) and Camden (rocket motors), the European architecture has single or near-single-source nodes at Bergerac/Sorgues/Pont-de-Buis (Eurenco energetics), Wimmis/Aschau (Nitrochemie propellants and energetics), Niedersachswerfen/Unterlüss (Rheinmetall filling and gun forging), Glascoed/Radway Green (BAE filling and small-arms) and Colleferro/Aulla (Italian energetics and propulsion). The European map has more nodes. It has, at the critical strategic-energetics layer, fewer producers per node than the American map.

5. The Ukraine Verdict, 2022–2026

The Ukraine 155 mm ammunition demand signal that emerged from February 2022 onward is the European equivalent of the March 2026 Iran War demand signal that produced the visible failure of the American precision-munitions base. The European demand signal is two and a half years older. It surfaced first because Continental Europe is geographically adjacent to the conflict, because Member States committed to ammunition contributions to Ukraine at scale, and because the United States 155 mm production estate, concentrated through Scranton (forgings), Iowa Army Ammunition Plant (filling) and Holston (energetics), cannot, by itself, source either the European Union’s commitments or the Ukrainian operational consumption rate.

On 20 March 2023 the Council of the European Union adopted the three-track ammunition plan: drawdown from Member State stocks, joint procurement of new ammunition, and ramp-up of European production capacity [9]. The headline target, set publicly by Internal Market Commissioner Thierry Breton, was the production of one million 155 mm rounds annually by March 2025. The European Union Act in Support of Ammunition Production (ASAP), Regulation (EU) 2023/1525, was adopted in July 2023 with a financial envelope of approximately €500 million, expressly aimed at accelerating production capacity through reverse public-private support to industry [10].

As of early 2025, the one-million target was missed on every credible producer and Member State assessment. The actual delivery against the Ukrainian-bound commitment in the year to March 2025 was variously assessed at between approximately 450,000 and 600,000 rounds, depending on the counting basis (commitments vs deliveries; new production vs drawdown vs joint procurement) [11]. Subsequent revisions through late 2025 indicated cumulative deliveries against the Ukraine commitment approaching, and on some tallies reaching or exceeding, one million rounds across the broader 2024–2025 window, with European new-build capacity rising toward the 1.7–2.0 million rounds-per-year range projected for end-2026.

The reasons for the original miss were not principally political will, nor financing. They were structural: insufficient energetics throughput at the Eurenco/Nitrochemie/Nammo layer; constrained filling capacity at the Rheinmetall, BAE, Nexter and Expal end of the chain; small numbers of qualified second sources; long lead time on new lines (Rheinmetall Niedersachswerfen, opened February 2025, was approximately twenty-four months from political announcement to opening of the first line, an industry-leading pace and not replicable across every Member State).

The Structural Lesson, Not the Counting Argument

The detailed counting of Ukraine-bound deliveries against the original European Union one-million-round target is politically contested. Several countings, including those of the European Commission and several Member States, present cumulative figures by late 2025 that approach or exceed the original target on broader bases. The structural diagnosis is independent of the counting outcome. The original target was set in March 2023; the first new energetics line capable of supplying the ramp at scale opened in February 2025. The two-year delivery lag is the cycle time of the rule layer. The shortfall, recovery and ongoing structural condition all express, at different points on the timeline, the same underlying property: a procurement system that had inverted its function across four prior waves cannot, on demand, deliver the surge capacity its original function presupposed. ASAP, EDIP and ReArm Europe operate at the appropriation layer. Without a parallel rule-layer change, the appropriations refill the architecture they were built to fund.

6. The European Counter-Models: Where Procurement Still Works

The Continental industrial base contains, alongside the inversion pattern, four counter-models. Each demonstrates that the inversion is a choice, not an iron law. Each is, in 2026, scaling faster than the consolidated mainstream.

6.1 Nammo: The Dispersed Multi-National Model

Nammo Group, formed in 1998 by the merger of the ammunition divisions of Raufoss Ammunisjonsfabrikker (Norway), Patria Vammas (Finland) and Celsius Försvarsmateriel (Sweden), is a deliberately dispersed multi-site producer [12]. Its corporate structure, fifty per cent owned by the Norwegian state and fifty per cent by Patria of Finland, was designed from inception to operate across multiple national jurisdictions, multiple regulatory regimes and multiple natural-disaster envelopes. Nammo today operates production sites at Raufoss (Norway, the corporate anchor), Vihtavuori (Finland, propellants), Karlsborg (Sweden), Vanasverken (Sweden), Belín (France, propulsion), Costa Mesa (United States), and other smaller facilities. The dispersal logic is explicit: no single national-level industrial event takes the company offline.

The Nammo model demonstrates that distributed industrial-base architecture is commercially viable. Nammo is profitable, growing, and exports across NATO and approved third countries. Its existence within Europe means the dispersed-redundancy architecture is not a theoretical option that requires invention; it is an operational pattern that requires extension. In the language of this piece: Nammo is what European procurement looks like when it has not yet inverted.

6.2 Czechoslovak Group: Horizontal Acquisition and the East European Capacity Layer

Czechoslovak Group (CSG), held by the Strnad family of the Czech Republic, has across 2014–2026 acquired a sequence of European ammunition, vehicle and small-arms firms: Excalibur Army, Tatra Defence Vehicle, Sellier & Bellot (small-arms ammunition), MSM Group (small- to medium-calibre, Slovakia), Fiocchi Munizioni (Italy, acquired 2022), Kinetic Group (Vista Outdoor ammunition portfolio, including Federal, Remington, Speer, CCI, acquired October 2024) [13]. The horizontal acquisition strategy has produced, in 2026, one of the largest single private ammunition holdings in Europe and one of the few firms capable of providing 155 mm ammunition at six- to eight-figure annual quantities under non-EU-Member-State sourcing arrangements (CSG’s Czech Initiative for Ukraine sourcing, beginning 2024, delivered substantial volumes from third-country production through Czech procurement channels).

6.3 Polska Grupa Zbrojeniowa: State-Holding Reconsolidation

Polska Grupa Zbrojeniowa (PGZ), formed by Polish parliamentary statute in 2013, brought several dozen Polish defence firms under a single state-holding structure (PGZ corporate disclosures variously list between forty and sixty entities depending on year and counting basis) [14]. The PGZ portfolio includes Mesko (ammunition and missiles), Zak&l;ady Mechaniczne Bumar-&L;abėdy (armoured vehicles), Huta Stalowa Wola (artillery), Pioma-Odlewnia (forgings), the Wojskowe Zak&l;ady portfolio and many others. PGZ is an explicit reconsolidation in the opposite direction of the Western pattern: from a fragmented post-Soviet industrial estate toward a coordinated state-holding architecture, designed to optimise for surge capacity, sovereign supply and strategic reserve. The PGZ model is, structurally, the closest European analogue to the Turkish SSB cluster pattern referenced in the original 11 May 2026 special report, achieved within the European Union rather than outside it.

6.4 Bofors–Saab Dynamics: The Vertical Integration Tradition

Saab AB’s Dynamics business area, anchored on the historic Bofors works at Karlskoga, retains a vertical integration tradition that runs from energetics through warhead, motor, guidance, integration and final assembly. The combination of Saab Dynamics, Saab Bofors Test Center, and the propellant-and-energetics work absorbed into Nammo Sweden AB in 2005 preserved a substantial fraction of the historic Bofors capability layer within Swedish industrial control. The Swedish national procurement model, operated through Försvarets Materielverk (FMV), has historically valued sovereign capability over price-only selection. The Saab Dynamics RBS-15, RBS-70, NLAW (jointly with Thales Air Defence at Belfast), Carl-Gustaf and Bill 2 product lines all draw on vertically-integrated production that did not pass through the same consolidation funnel that hollowed the Anglo-French production estates.

Taken together, the four counter-models show that European Union rule-layer reform does not need to import the Turkish model from outside the Alliance. It has working European models inside it — a dispersed multi-national producer (Nammo), a horizontal acquirer with active global sourcing (CSG), a state-holding reconsolidation (PGZ) and a vertical-integration national model (Saab–Bofors–Nammo Sweden). Each scaled faster across 2022–2026 than the consolidated mainstream.

7. The European Union Response: Money Against an Inverted Function

The European Union response to the 2022–2026 industrial-base reckoning has run on three named instruments. ASAP, EDIP and ReArm Europe operate at the appropriation layer. They do not, on present drafting, rewrite the source-selection rule that produced the inverted architecture.

7.1 ASAP, Act in Support of Ammunition Production

Regulation (EU) 2023/1525 of 20 July 2023 established ASAP with an initial envelope of €500 million for the period to 30 June 2025 [15]. ASAP grants supported industrial capacity expansion principally in 155 mm artillery ammunition, energetics and missiles. The grants disbursed across 2023–2025 went to consortia of European industry actors, with reporting under the Regulation indicating disbursements to projects led by Eurenco, Rheinmetall, Nammo, Nexter, CSG, Expal, MBDA and others. The instrument was, on its own terms, successful in unblocking some short-term capacity. It did not, by design, change the rule under which the next procurement cycle awards contracts.

7.2 EDIP, European Defence Industry Programme

The European Defence Industry Programme proposal, published by the European Commission on 5 March 2024, is the longer-term successor framework [16]. EDIP envisaged sustained Union financial support to European industry, mechanisms for joint procurement, and instruments to encourage industrial cooperation. EDIP’s passage through the Council and Parliament has been protracted; the final shape, financial envelope and governance arrangements were, as at May 2026, subject to ongoing negotiation, with national positions varying significantly on the questions of whether non-Union-Member-State suppliers should qualify, what fraction of disbursements should require minimum Union content, and whether Union industrial planning should bind national procurement decision-making.

7.3 ReArm Europe and SAFE

The ReArm Europe plan, announced by the European Commission in March 2025, proposed a substantially larger financing envelope, a stated up-to-€800 billion across the planning horizon, combining national fiscal flexibility under State aid rules, European Investment Bank instruments, and a new Security Action for Europe (SAFE) loan facility [17]. ReArm Europe is the largest financial mobilisation in the European industrial-base history of the Union. It is, again, an appropriation-layer instrument. Its drafting did not rewrite Directive 2009/81/EC. It did not mandate surge capacity as a Union-level award criterion. It did not require dual-qualification of strategic-energetics sources. It did not establish a Union-level strategic energetics reserve. It funded the architecture.

7.4 What the Union Response Did Not Do

The structural observation is consistent across the three instruments. Each disbursed money. None changed the rule under which a Member State procurement official, in 2026 or 2027, awards a contract. Until the rule layer changes, until Directive 2009/81/EC Article 47 is amended to require, in defence and security procurement above a stated threshold, mandatory evaluation of surge capacity, dual qualification and strategic-input redundancy, the appropriation layer continues to fund the architecture that produced the shortfall it is meant to address. Money administered through an inverted function buys more of the inversion.

8. Restoring Procurement: What Reform Would Look Like

The question of how to restore procurement to its original function, asked of the European Union, has a substantively different answer from the question asked of the United States. The Union rule layer is younger (2009 versus FAR Part 15 1997). The Member State rule layers are older and remain partially insulated by TFEU Article 346. The institutional vehicles available for Union-level reform, Commission proposal, Council and Parliament co-decision, Member State transposition, are different from the United States legislative path. The substantive content of reform is, however, recognisably parallel.

| Reform element | Existing Union authority & supporting STANAG / AOP | Indicative lead time [ISC Estimate] | Principal obstacle |

|---|---|---|---|

| Lead-time column — ISC analytical estimate, indicative only. Year-ranges reflect ISC’s assessment of standard EU co-decision timelines (3–5 years), NATO STANAG ratification cycles (typically 3–6 years), Member State transposition windows (typically 2 years post-Directive), and observed lead times on comparable industrial-base instruments (DPA Title III analogues; ASAP disbursement cycles). Specific timelines for any individual proposal will depend on political circumstance and are not forecast here as event predictions. | |||

| Amend Directive 2009/81/EC Article 47 to mandate surge-capacity evaluation in defence and security procurement above stated threshold | TFEU ordinary legislative procedure; Commission proposal required | 3–5 years from proposal to Member State transposition | Member State opposition under Article 346 doctrine; concern over national-champion ringfencing erosion |

| Establish Union-level Strategic Energetics Reserve, financed under SAFE / EDIP successor, held at dispersed sites under NSPA stewardship | EDIP framework if adopted with this scope; NSPA host-nation arrangements; STANAG 4439 / AOP-39 storage standards for IM-compliant fills | 5–7 years to first operational reserve at meaningful scale | Cost (€25–60 billion order-of-magnitude); host-nation acceptance of risk; energetics ageing protocol |

| Mandate dual qualification of HD 1.1 / Hazard Division 1.1 strategic energetics across Member State procurement | Council framework decision; STANAG 4170 / AOP-7 (Manual of Tests for the Qualification of Explosive Materials for Military Use); NSPA host-nation programme | 3–5 years from decision to first qualified second-source production at scale | Cost premium of approximately 8–15 per cent on protected items; industry coordination across multiple producers |

| Re-weight MEAT criteria across Union defence and security procurement to give industrial-base resilience a stated minimum weight (indicative 20–30 per cent) | Directive 2009/81/EC Article 47 secondary legislation; Commission Implementing Acts; Member State transposition | 2–4 years | Member State sovereignty over award criteria; price-only legacy in low-margin procurement; potential WTO Government Procurement Agreement interactions |

| STANAG-level surge framework: mandatory surge clauses, minimum standby capacity, geographic dispersion in NATO contracts | NATO Conference of National Armaments Directors (CNAD); NSPA; STANAG 4107 / AQAP-2110 series (Allied Quality Assurance Publications) for surge-clause enforceability | 3–6 years through STANAG process | Existing AC/327 (LCMG) versus AC/326 (CASG) competence gap; Member State price discipline; absence of mandatory STANAG enforcement mechanism |

The five elements are mutually reinforcing. None replaces the others. None obviates ASAP, EDIP or ReArm Europe at the appropriation layer; they operate at a distinct rule layer that the appropriation instruments do not address. Together they describe what reversing the inversion would require: a return to the explicit treatment of industrial-base resilience as a constitutive obligation of the procurement function, codified in Union law, given technical content through the STANAG suite, and operationalised through dual-qualified, dispersed, surge-capable production at the strategic-input layer.

9. Caveats and Boundaries

This analysis is open-source, unclassified, and explicit about what it does and does not establish.

It does not assert that lowest-price selection is wrong in every domain. For commodity items, fungible goods and contractually well-bounded services, lowest-price selection within a defined technical specification is an efficient and proportionate rule. The argument is narrower: in defence procurement at the strategic-input layer (energetics, propellants, large-calibre forgings, seeker assemblies, solid rocket motors), where qualified-source counts are small and lead times to add a second source run twenty-four months and longer, lowest-price selection produces single-point-of-failure industrial concentration.

It does not establish that the Union response has failed. ASAP unblocked specific capacity. EDIP, if passed in a meaningful form, will direct sustained Union investment. ReArm Europe is, on its scale, unprecedented. The argument is that none of these instruments, as drafted, rewrites the source-selection rule. The appropriation layer and the rule layer are separate, and the rule layer is what produced the structural concentration.

It does not assert that consolidation was uniformly destructive. The Rheinmetall, KNDS, Eurenco and MBDA consolidations produced firms capable of substantial European-scale industrial activity. The argument is that consolidation without retained dispersed surge capacity, retained dual qualification and retained strategic reserve produces a structure whose efficiency is its vulnerability.

The orders of magnitude indicated in Section 8 are illustrative and would require detailed analysis under the same Belcher, Rasmussen, Kemshaw and Zornes (2016) transdisciplinary research-quality framework applied in the United States special report companion to this piece. Specific monetary figures for a Union-level Strategic Energetics Reserve, a re-weighted MEAT criterion, or a STANAG-level surge framework would all require Member State and Commission costing work that this piece does not perform. The “function inversion” frame deployed throughout is ISC’s own analytical coinage; it is not drawn from a third-party framework.

Data gaps. Specific Member State 155 mm production figures for the year to March 2025 vary by counting basis; the published European Commission, Council and Member State assessments do not always align. The energetics throughput of Nitrochemie at Wimmis and Aschau is reported in industry trade press but not consistently in formal Union statistical publications. The Royal Naval Armament Depot residual operational footprint as at 2026 is partially classified and reported only in aggregate by the United Kingdom Ministry of Defence and Defence Equipment & Support (DE&S).

10. Source Evaluation

Sources for this analysis are evaluated using the NATO STANAG 2022 Reliability (A–F) and Accuracy (1–6) framework, with the overall product rated A–2 (reliable origin, probably true content). Source tiers used:

- Tier 1, Treaty texts, Union legislation, Member State statutes, NATO publications: Directive 2009/81/EC; TFEU Article 346; Regulation (EU) 2023/1525 (ASAP); United Kingdom Defence and Security Public Contracts Regulations 2011; STANAG 4107, STANAG 4170 / AOP-7, STANAG 4439 / AOP-39; AQAP-2110; United Kingdom Ministry of Defence Defence Equipment Plan annual returns; French DGA annual reports; German BAAINBw published procurement notices.

- Tier 2, Government audit and oversight publications: United Kingdom National Audit Office reports on Royal Ordnance privatisation and MASS/NGMS; European Court of Auditors reports; House of Commons Defence Committee reports; French Cour des Comptes reports on DGA and GIAT.

- Tier 3, Named-expert think-tank analysis: Royal United Services Institute (RUSI); International Institute for Strategic Studies (IISS); German Institute for International and Security Affairs (SWP); Institut Français des Relations Internationales (IFRI); Istituto Affari Internazionali (IAI); European Council on Foreign Relations (ECFR); Bruegel; CSIS (US-domiciled; applied where European-relevant).

- Tier 4, Specialist defence press: Jane’s Defence Weekly; Defense News; Shephard Media; Naval News; Hartpunkt; European Security & Defence; Bruxelles2.

- Tier 5, Industry primary disclosures: Rheinmetall AG annual reports and trading updates; KNDS Group disclosures; BAE Systems plc annual report; Nexter / KNDS communications; Eurenco corporate communications; Nammo Group annual reports; Saab AB annual reports; CSG corporate communications.

STANAG 2022 ratings inline are applied to contested or specific quantitative claims. The aggregate rating reflects the consistent direction of evidence across tiers, with residual data gaps identified explicitly in Section 9.

11. ISC Commentary

ISC Defence Intelligence assesses that the European defence industrial base will not become structurally resilient as a function of appropriation alone. The instruments now in flight, ASAP closed in mid-2025, EDIP under co-decision, ReArm Europe and SAFE in early implementation, deploy money against a procurement architecture that was produced, across four decades, by source-selection rules that valued lowest peacetime price over capability delivery. Money administered through those same rules buys more of the inverted architecture. It does not change the inversion.

The rule layer, in the European Union and at Member State level, has not changed. Directive 2009/81/EC Article 47 still permits lowest price or MEAT. The Member State implementing legislation has not, in any major Member State, mandated surge capacity as an evaluation factor. The NATO Support and Procurement Agency’s International Competitive Bidding “L1” lowest-compliant selection persists at the Alliance level. The Royal Naval Armament Depot footprint is not being restored. The Royal Ordnance Factory estate is not being reconstituted. The Heeresmunitionsanstalten are not being reopened. The Pirotecnici are not being reactivated. None of those moves is being seriously contemplated within the current Union policy frame.

That is the structural diagnosis. The European arsenal of 1945 was a mesh, by design, under cost-plus accounting and under sovereign industrial policy. It was inverted across four waves between 1957 and 2009 under four different rule shifts, the United Kingdom Sandys White Paper, the French GIAT corporatisation, the British Aerospace acquisition of Royal Ordnance, and Union Directive 2009/81/EC. Each wave reduced redundancy and rewarded consolidation. Each wave was a rational response by industrial actors to the rule each Government and the Union set. None of the four waves abolished the procurement function in name. Each of the four waves inverted what the procurement function, in practice, produced.

The Ukraine 155 mm demand signal of 2022–2026, like the March 2026 Iran War for the United States, is not the cause of the problem. It is the visible verdict on what the inverted function built. The next visible verdict will arrive at the time of the next scenario the rules did not provide for. That timeline is no longer the prerogative of European policy planners.

The reform path is known. It runs through Directive 2009/81/EC Article 47 amendment. It runs through Member State transposing legislation. It runs through NATO STANAG 4107 / AQAP-2110 implementation guidance, STANAG 4170 / AOP-7 qualification protocol, and STANAG 4439 / AOP-39 IM compliance. It runs through the establishment of a Union-level Strategic Energetics Reserve and through a STANAG-level surge framework. It does not require the invention of new institutions; the Conference of National Armaments Directors, the European Defence Agency, the NATO Support and Procurement Agency, the Allied Committee 326 and 327 structures and the Member State armaments directorates already exist. What is missing is the rule change those institutions would administer.

Until that rule change is on the table at the European Commission and at the North Atlantic Council, the structural condition of the European defence industrial base in 2026 is the structural condition that produced the 2025 ammunition shortfall. The instruments that funded the shortfall’s correction operate at a layer separate from the layer that produced it. Both layers will need to move. On present trajectories only one is moving.

The word for the activity now performed by Brussels, London, Paris, Berlin and Rome under the heading defence procurement is not, strictly, procurement. The function has inverted; the name remains.

References and Sources

- Tier 2 United Kingdom National Audit Office and House of Commons Public Accounts Committee reports on Royal Ordnance and the Royal Ordnance Factory estate, 1984–1990 (multiple reports cited collectively for the forty-two-site peak figure confirmed by contemporary parliamentary returns). www.nao.org.uk · Hansard archives

- Tier 1/2 United Kingdom Ministry of Defence and Royal Navy historical estate publications; Defence Estates and Defence Infrastructure Organisation site lists; Imperial War Museum collection records for individual RNAD sites including Priddy’s Hard, Bedenham, Bull Point, Crombie, Ernesettle, Glen Douglas, Coulport, Trecwn, Dean Hill, Beith and Broughton Moor. DIO · IWM

- Tier 1 United Kingdom Defence White Paper, “Defence: Outline of Future Policy” (Cmnd. 124), April 1957, Duncan Sandys, Minister of Defence. Hansard, 17 April 1957

- Tier 2 French Cour des Comptes annual reports on GIAT Industries; French Senate and National Assembly defence-committee reports 1990–2010; subsequent Nexter and KNDS press releases on workforce evolution and recapitalisation. Cour des Comptes

- Tier 2 National Audit Office, “Sale of Royal Ordnance plc,” HC 162 of Session 1986–87, 1987; House of Commons Public Accounts Committee proceedings; British Aerospace plc annual reports 1987–1990. NAO archive

- Tier 2 National Audit Office assessment of the £190 million sale price including subsequent valuations of the property portfolio and intellectual property; cross-referenced with Hansard parliamentary debate of 23 April 1987.

- Tier 1/4 United Kingdom Ministry of Defence Munitions Acquisition and Supply Solution (MASS, 2008) and Next Generation Munitions Solution (NGMS, 2023) contract notifications; BAE Systems Land UK plc publications; specialist defence press reporting (Janes, Defence News UK). DE&S

- Tier 1 Directive 2009/81/EC of the European Parliament and of the Council of 13 July 2009 on the coordination of procedures for the award of certain works contracts, supply contracts and service contracts by contracting authorities or entities in the fields of defence and security. EUR-Lex CELEX 32009L0081

- Tier 1 Council of the European Union conclusions, 20 March 2023, Foreign Affairs Council (Defence) on the three-track ammunition plan for Ukraine. Council conclusions, March 2023

- Tier 1 Regulation (EU) 2023/1525 of the European Parliament and of the Council of 20 July 2023 on supporting ammunition production. EUR-Lex CELEX 32023R1525 (ASAP)

- Tier 2/3 European Commission, Council and Member State public reporting on Ukraine-bound ammunition deliveries; Estonian, German, Czech and French national reporting; RUSI, IISS, ECFR, Bruegel and SWP analyses (2023–2025) of the three-track plan’s delivery against target, including subsequent late-2025 cumulative assessments.

- Tier 5 Nammo Group annual reports and corporate history publications, Raufoss; www.nammo.com.

- Tier 4/5 CSG corporate communications; specialist defence press reporting on CSG acquisitions including Sellier & Bellot, Fiocchi Munizioni (2022), Kinetic Group (Vista Outdoor Sporting Products, October 2024). CSG

- Tier 1/5 Polish parliamentary statute establishing PGZ (2013); PGZ corporate communications; grupapgz.pl.

- Tier 1 Regulation (EU) 2023/1525 (ASAP) financial envelope and disbursement reporting; European Commission Directorate-General for Defence Industry and Space (DG DEFIS) updates. DG DEFIS

- Tier 1 European Commission, “Proposal for a Regulation of the European Parliament and of the Council establishing the European Defence Industry Programme,” COM(2024) 150 final, 5 March 2024. EUR-Lex CELEX 52024PC0150 (EDIP)

- Tier 1 European Commission, “ReArm Europe” communication and the Security Action for Europe (SAFE) instrument proposal, March 2025; subsequent Council conclusions on European Defence financing. DG DEFIS, ReArm Europe

- Tier 1 NATO STANAG 4170 / AOP-7, Manual of Tests for the Qualification of Explosive Materials for Military Use; STANAG 4439 / AOP-39, Policy for Introduction and Assessment of Insensitive Munitions; STANAG 4107 / AQAP-2110, NATO Quality Assurance Requirements for Design, Development and Production. NATO Standardization Office

Companion references: ISC Defence Intelligence, “Lowest-Bid Procurement: Dismantling the Western Industrial Base” (11 May 2026) and “Lowest-Bid Procurement: Special Report” (11 May 2026). This piece is the European/EU companion to those analyses, written under the function-inversion frame.