Graphic: ISC Defence Intelligence. Channels and manufacturer roles compiled from EU TED notices 353940 and 354489-2026, NSPA and Rheinmetall.

Same Old Story: EDA Procurement, Framework Collisions and the West's Through-Life Reckoning

The Order Book

On 26 May 2026 the European Defence Agency (EDA) published two ammunition procurement notices in the Official Journal, indexed in Tenders Electronic Daily as 353940-2026 and 354489-2026, both carrying the single internal identifier CPoA B PRJ.CAP.1269 2026. The first seeks 155mm artillery ammunition, as complete All Up Rounds and as individual components, split into 24 lots across two gun platforms: the wheeled CAESAR and the tracked PzH2000. The second seeks small arms and auto-cannon ammunition in 19 lots spanning the 5.56mm x 45, 7.62mm x 51, 9mm x 19, 12.7mm x 99 and 30mm x 173 natures. Forty-three lots in total, one request-to-participate deadline of 10 June 2026, and a single contracting mechanism stated in identical words on every lot: framework agreement, without reopening of competition.

This is the latest tranche of a buying programme that has run hard since 2023. In March that year, EU Member States and Norway signed a seven-year framework arrangement letting the EDA coordinate joint ammunition procurement to replenish national stocks and to backfill what has gone to Ukraine. The Agency has since signed framework contracts for 155mm and widened the aperture: its 2025 Annual Report records procurement concentrated on 155mm and on 84mm Carl Gustaf ammunition, with collaborative 155mm orders worth more than 375 million euros running under the Collaborative Procurement of Ammunition project, itself funded through the European Defence Industry Reinforcement through common Procurement Act (EDIRPA). Above it all sits the European Defence Industry Programme (EDIP), adopted by Council on 8 December 2025, carrying 1.5 billion euros for 2026 to 2027 and a security-of-supply regime first debated inside the EDA. The new notices reach deeper into the supply chain than a buyer normally goes. The 155mm tender does not just call for finished rounds; it tenders the fuzes, the projectiles, the Modular Charge System top and bottom charge modules, and the primers as separate lots. On paper this is exactly what the post-2022 reviews demanded: aggregate the demand, sign the frameworks, fund the ramp-up. The problem is what the order book runs into.

Forty-three lots, one deadline, and the same line on every one: framework agreement, without reopening of competition. The contract does not manufacture anything. It allocates a place in a queue, and the EDA, the NSPA and the national frameworks are all queueing for the same shells, the same propellant and the same explosive fill. ISC Defence Intelligence assessment

Parallel Channels: EDA, NSPA and National Frameworks

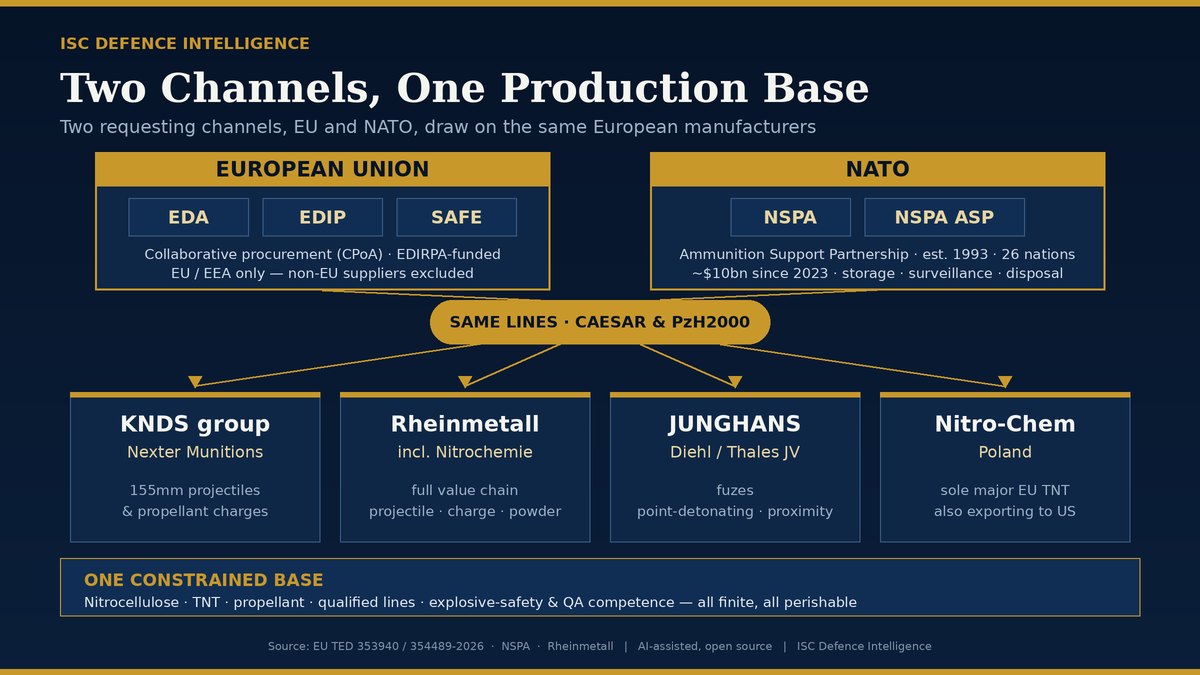

A framework contract is a purchasing instrument, not a factory. It fixes price, terms and a roster of qualified suppliers, and it lets a buyer call off quantities quickly. What it cannot do is conjure throughput the physical base does not have. The sharper point is that the EDA channel is only one of several frameworks aimed at the same guns, the same primes and the same lines. The 26 May notices tender 155mm rounds and components for the CAESAR and the PzH2000. Those are the same two platforms named in the framework the NATO Support and Procurement Agency (NSPA) signed in January 2024, when it placed contracts worth 1.1 billion euros with Nexter Munitions, part of the Franco-German KNDS group, and the fuze maker JUNGHANS, for around 220,000 rounds of 155mm ammunition and fuzes. Nexter supplies the projectiles and propellant charges; JUNGHANS supplies the fuzes. The EDA is now tendering those same component families for those same platforms.

Around that overlap sit several more demand streams. National replenishment runs through the NATO Defence Planning Process, with each ally rebuilding war stocks against agreed capability targets and calling off from broadly the same base. The Security Action for Europe (SAFE) instrument will lend up to 150 billion euros to Member States by 2030, much of it likely to land on existing munitions. Ukraine is supplied through EU instruments, the EDIP Ukraine Support Instrument and direct national donation. The NSPA route is itself large: its Ammunition Support Partnership, set up in 1993 and now numbering 26 nations, has agreed roughly 10 billion dollars of contracts since NATO adopted its Defence Production Action Plan in July 2023, and it explicitly bundles ammunition storage, transport, surveillance and disposal alongside supply. Sovereign national frameworks add more. In June 2024 the German Bundeswehr extended a 155mm framework with Rheinmetall to a gross ceiling of up to 8.5 billion euros, the largest order in that company's history, with deliveries also routed to Ukraine, the Netherlands, Estonia and Denmark. A quieter pull is export: Poland's Nitro-Chem, the only major trinitrotoluene (TNT) producer in Europe, has committed multi-year TNT supply to United States artillery programmes under a contract reported at 310 million dollars. Nations sit in several of these channels at once, and no published mechanism stops one loading line or energetics plant taking parallel calls-off from an EDA framework, an NSPA framework, a national framework and Ukraine backfill in the same window. This is not coordination. It is parallel demand bidding for one set of lines.

Two consequences follow. The first is concentration. The qualified primes that already hold the big frameworks, the KNDS group's Nexter lines in France and Germany, Rheinmetall, and fuze and energetics specialists such as JUNGHANS and Rheinmetall's Nitrochemie propellant arm, are the same firms positioned to win the EDA component lots, because they hold the qualified lines and the live approvals. Vertical integration deepens the moat, with Rheinmetall buying into nitrocellulose through Hagedorn-NC and Colt CZ taking control of Synthesia. The second is exclusion. Both 26 May notices state that participation is open on equal terms only to entities registered in the European Union and the European Economic Area, and that the World Trade Organization Government Procurement Agreement and the EU-UK Trade and Cooperation Agreement do not apply to EDA procurement. United Kingdom, United States and other non-EU suppliers are shut out of the EDA channel by rule, even where they sit inside the same NATO supply chains served by the NSPA. EU money is being ring-fenced to a concentrated, largely Franco-German industrial core at the same moment that core is the binding constraint. Shut out of the EDA route, non-EU primes can still reach the same market through NATO via the NSPA, which holds non-EU allies such as the United Kingdom, the United States and Turkey, or bilaterally, which pushes them toward the very channel already competing with the EDA for the same lines.

Stack these parallel channels onto one constrained base and the binding limit is not the contract paperwork. It is the energetics. Artillery output is gated less by steel casings than by propellant and high explosive. European nitrocellulose production sits at roughly 4,500 to 10,000 tonnes a year against estimated combined European and Ukrainian need of about 20,000 tonnes, a shortfall of up to 14,000 tonnes a year. The new nitrocellulose and TNT plants funded to close that gap are not all in full operation, with several not expected to mature until 2026 and beyond. Industry has moved to buy its way up the supply chain, with Rheinmetall acquiring the nitrocellulose producer Hagedorn-NC in April 2025 and Colt CZ taking a controlling stake in Synthesia Nitrocellulose in January 2026 for around 870 million euros. Those are sound moves. They do not change the arithmetic this year. Adding another framework call-off to a base that is already energetics-limited does not produce more ammunition. It lengthens the queue and bids up the unit price, the precise outcome that aggregated demand was supposed to prevent.

Mandate: Coordinator, or Buying Agent?

So what is the EDA actually for? Its founding statute, Council Decision (CFSP) 2015/1835, casts the Agency primarily as a facilitator and coordinator. Its functions and tasks, set out in Article 5, centre on identifying shared priorities, harmonising military requirements, promoting procurement best practice and proposing collaborative projects, and it is expected to prepare programmes for management by others, including the Organisation for Joint Armament Cooperation (OCCAR). The statute does let the Agency go further. For ad hoc projects and programmes that participating Member States approve and fund, it may manage the budgets and enter the necessary contracts under EU procurement rules. The consistent thread is that the Agency's value is meant to lie in coordination, harmonisation and programme management. It was not designed as a standing buying agent placing orders that Member States or other bodies could place themselves.

The 2024 Long-Term Review pushed hard in the procurement direction. On 28 May 2024 EU defence ministers raised the Agency's core tasks from three to five and added, in their own words, "aggregating demand towards joint procurement to fill capabilities shortfalls", confirming that the EDA can support every step of the capability cycle, including off-the-shelf acquisition where Member States decide. The 2023 155mm framework contracts were the proof of concept. The 26 May 2026 notices are that model scaled up and pushed down to component level.

This is where the direction of travel sits awkwardly with the Agency's own design. A body created to harmonise demand and to hand complex procurement to OCCAR or the NSPA is now running its own component-level framework competitions for fuzes, projectiles, charge modules and primers, on the very platforms, the CAESAR and the PzH2000, where the NSPA already holds a framework with the same primes. A defender will point to the ad hoc project provisions and the 2024 mandate and say this is squarely authorised, and on the letter of the rules that is correct. The harder question is whether it is consistent with the purpose. The statute's test is added value through coordination, and that value is difficult to see when a second European institution opens parallel calls-off against the same constrained lines the NSPA is already buying from, with no published mechanism to de-conflict the two. Demand that is split across rival EU and NATO channels at the same time has not been aggregated. It has been duplicated, in the language of cooperation. That is the clearest single sign that Europe's ammunition problem is structural rather than passing: the institutions built to cure fragmentation are now adding to it.

Who Verifies the Technical Compliance?

Buying ammunition is not the same as assuring it. A 155mm framework that tenders fuzes, projectiles, charge modules and primers as separate lots needs technical oversight at a level most procurement officials do not hold: Allied Quality Assurance Publication (AQAP) 2110 quality approval at each supplier, Government Quality Assurance under Standardisation Agreement (STANAG) 4107 and its mutual process AQAP-2070, and ammunition-specific judgement on hazard classification, net explosive quantity, energetic fill and fuze safety. Under STANAG 4107 that Government Quality Assurance is a national responsibility, performed by a Member State's national quality assurance authority and delegated between nations, not something the contracting body discharges itself. The people who carry this competence are Weapons, Ordnance, Munitions and Explosives (WOME) specialists: ammunition technical officers, explosives safety practitioners, AQAP auditors and surveillance chemists.

This is exactly the competence the NSPA pools. The Ammunition Support Partnership exists to provide storage, transport, surveillance and disposal as well as supply, which means it is staffed with WOME-competent technical personnel who are placed to watch a procurement of this kind and confirm that it is technically compliant and aligned with the AQAP quality framework. The open question is what equivalent sits inside the EDA channel. The Agency's statutory role is coordination and harmonisation, not Government Quality Assurance, and the public record does not show that it holds an in-house WOME and AQAP-qualified cadre of its own. So when the EDA signs a 24-lot, two-platform framework open to suppliers across the European Union and the European Economic Area, who performs the Government Quality Assurance, which national authority is delegated to do it, and how is that de-conflicted against the parallel NSPA and national contracts on the same lines? None of this is published.

There is a deeper loop that nobody appears to close. ISO 9001, the standard the AQAP suite is built on, requires an organisation to determine and assure the competence of the people whose work affects quality, yet it does not define what that competence is for any sector. If the EDA is now a contracting authority for ammunition, the same test applies to its own staff. Who verifies that EDA procurement personnel are competent to specify, evaluate and manage WOME contracts, and against what defined standard? The NATO body that owns the quality framework, the Life Cycle Management Group (AC/327), and the body that owns ammunition safety, the Conventional Armaments Safety Group (AC/326), sit apart, and neither closes that loop for procurement staff. The risk is a procurement that is administratively sound and technically unattended, with the people best qualified to monitor it sitting in the other channel.

The Storage and Through-Life Reckoning

Assume the West succeeds, and the lines do scale. A second problem then arrives on a delay timer. A surge that fills magazines in a compressed window pushes a very large cohort of ammunition into service at roughly the same time. Ammunition does not sit inert. Propellants based on nitrocellulose degrade through stabiliser depletion, a time and temperature dependent process; the stabiliser, typically a compound such as diphenylamine, is consumed as it mops up the products of slow decomposition. Once it is exhausted, decomposition can become self-accelerating, which is why in-service surveillance and proof exist and why propellant has a managed shelf life. Surveillance programmes track the remaining stabiliser content lot by lot to forecast when each must be proofed, life-extended or disposed of.

A synchronised intake produces a synchronised output of decisions. Roughly a decade after the surge, a single large tranche reaches its surveillance and life-assessment gates together, and the West faces a simultaneous wave of proof, life-extension and disposal judgements rather than the smooth annual flow a steady order book would have produced. The parallel channels make this worse rather than better: EDA, NSPA and national surges that fill magazines in overlapping windows produce several large cohorts arriving at their gates on similar timelines, concentrating demand on the same scarce surveillance chemists, proof facilities and disposal capacity at the same moment. That wave lands on a storage estate that took its own peacetime cuts. Licensed magazine capacity is finite and governed by net explosive quantity (NEQ) limits and the quantity-distance rules in the NATO storage and transport safety standards (the AASTP series). New stock needs licensed space, qualified storehouses and surveillance throughput, all of which have to be funded and manned. The demilitarisation and disposal bill, meanwhile, will fall due when the political emergency has passed and the budgets have relaxed. Through-life management is the cost that procurement headlines never mention and that the surge is quietly enlarging. This is building just as the first international instrument dedicated to the problem takes shape: the United Nations General Assembly adopted the Global Framework for Through-life Conventional Ammunition Management in December 2023, fifteen objectives spanning surveillance, storage and disposal, and States met in June 2025 to prepare for an implementation meeting in 2027 at which industry sits as an observer. The framework names the obligation. The current wave of framework buying does not visibly price it in.

When the Certificates Time Out

The sharpest edge is on the manufacturers, and it is a competence problem rather than a tooling one. The new and expanded lines funded under the Act in Support of Ammunition Production (ASAP) and adjacent instruments do not simply need machines. They need a live explosive safety case for each site and process, a current site explosives licence, and Allied Quality Assurance Publication (AQAP) approval, principally AQAP-2110, held under the framework of Standardisation Agreement (STANAG) 4107. None of these are one-time certificates. They are perishable. A safety case rests on a defined process, a licensed facility and trained, currency-maintained people. Quality approval rests on continuing production, audit and competent staff. Stop the work and the qualification does not pause politely; it lapses. The component-level structure of the 26 May 155mm tender makes the exposure concrete. A fuze line, a projectile line, a charge-module line and a primer line are each a distinct qualified supplier carrying its own safety case and its own AQAP approval, and each one runs down on its own clock the moment the calls-off stop. Parallel NSPA and national frameworks compound the exposure, because they draw on the same primes and the same approved lines, so a single supplier can be carrying overlapping calls-off whose certification clocks all run down together when demand softens.

This is the trap the West is building for itself. The surge stands up capacity, certifies it, and runs it hard while the political will and the money are present. When the conflict cools and the order book thins, the lines idle, the trained explosive safety and quality assurance personnel disperse to other work, supplier qualifications expire and the energetics base contracts back toward its peacetime floor. Re-establishing it later means repeating the cold start of 2022: re-qualifying suppliers, rewriting safety cases, re-licensing sites and rebuilding scarce specialist competence from a standing start. The West ends the crisis with the same fragile, hollow base it entered with, having spent heavily to arrive back where it began.

Personnel and Safety Considerations

Explosive safety and quality assurance competence is the West's true single point of failure, ahead of any individual factory. Ammunition technicians, explosives safety practitioners, AQAP auditors and surveillance chemists are produced slowly and lost quickly. A demand profile that spikes and then collapses is the worst possible environment for retaining them, because it offers neither the steady workload that keeps skills current nor the long-horizon employment that justifies training the next cohort. The synchronised surveillance wave described above will also concentrate demand for exactly these scarce people at exactly the moment the surge has dispersed them. Any honest readiness plan has to treat this human and certification base as a sustained-funding line, not a tap to be opened in war and shut in peace.

Data Gaps

Several figures central to this assessment are not in the open record and should be treated as gaps rather than findings. The split of EDA-coordinated tonnage between national stock replenishment and Ukraine backfill is not published at nature level. The real-world spare throughput of the new ASAP-funded energetics plants, as opposed to their nameplate capacity, is not independently verified. The exact NEQ headroom across allied licensed storage estates is not public. The age profile and stabiliser status of stock already delivered in the 2023 to 2026 surge, which would let the synchronised-surveillance forecast be quantified, are held nationally and not released. Neither 26 May notice publishes a total contract value or a guaranteed quantity, which is normal for a framework agreement where volumes are fixed later through individual calls-off; the per-lot turnover figures in the notices are tenderer eligibility thresholds and should not be read as contract values. Both notices are change notices correcting earlier May publications, so lot structures may yet move before the 10 June deadline. How the EDA, NSPA and national frameworks are de-conflicted against one another, and how much of each prime's order book is already committed, is not disclosed, so the true depth of the queue on any one line cannot be measured from open sources.

References

Source-evaluated under NATO STANAG 2022 (Reliability A–F / Accuracy 1–6). Tier 1 = government primary source; Tier 2 = quality news / specialist defence media; Tier 3 = authoritative aggregator / think-tank analysis.

- T1EU Tenders Electronic Daily (TED), buyer European Defence Agency: Supply of 155mm artillery ammunition (All Up Rounds and components), 24 lots, CAESAR and PzH2000, CPoA B PRJ.CAP.1269 2026, OJ S 99/2026, 26 May 2026. (Reliability A / Accuracy 1)

- T1EU Tenders Electronic Daily (TED), buyer European Defence Agency: Supply of Small Arms and Auto Canon Ammunition, 19 lots, CPoA B PRJ.CAP.1269 2026, OJ S 99/2026, 26 May 2026. (Reliability A / Accuracy 1)

- T1European Defence Agency: EDA Annual Report 2025 (procurement of 155mm and 84mm ammunition; demand aggregation), 2026. (Reliability A / Accuracy 1)

- T1European Parliament (EPRS): EU joint defence procurement (2023 seven-year EDA ammunition framework arrangement), 2026. (Reliability A / Accuracy 1)

- T1Council of the European Union: Council Decision (CFSP) 2015/1835 defining the statute, seat and operational rules of the European Defence Agency (Article 5 functions and tasks; ad hoc projects and programmes), 12 October 2015. (Reliability A / Accuracy 1)

- T2Army Technology (Salerno-Garthwaite): EDA adds joint procurement in Long-Term Review 2024 (three core tasks to five; aggregating demand towards joint procurement; whole-project support incl. off-the-shelf), 28 May 2024. (Reliability B / Accuracy 2)

- T1UN Office for Disarmament Affairs (UNODA): Global Framework for Through-life Conventional Ammunition Management (adopted by UN General Assembly December 2023; 15 objectives; A/78/111; Preparatory Meeting of States June 2025), 2023–2025. (Reliability A / Accuracy 1)

- T1Rheinmetall AG (company press release): Framework contract for 155mm artillery ammunition for the Bundeswehr, gross value up to 8.5bn euros, 20 June 2024. (Reliability A / Accuracy 1)

- T2Global Defense and Aerospace Post: NSPA procures 220,000 rounds of 155mm ammunition under DPAP (1.1bn euros, Nexter/KNDS and JUNGHANS; ASP since 1993; ~10bn dollars since July 2023), 25 January 2024. (Reliability B / Accuracy 2)

- T3Istituto Affari Internazionali (Murgia and Marrone): The European Defence Industry Programme: The Last Piece of the EU Defence Puzzle? (EDIP, SAFE, security of supply), 2 February 2026. (Reliability B / Accuracy 2)

- T3SETA Foundation (Ahmedoglu): Europe's Struggle: Cheap Weapons at Scale (nitrocellulose and TNT bottlenecks; Nitro-Chem; ASAP), 14 February 2026. (Reliability B / Accuracy 2)

- T3Beyond the Horizon ISSG: The European Defence Agency in 2025 (155mm CPoA orders over 375m euros; demand aggregation), 19 April 2026. (Reliability B / Accuracy 2)

Corrections & updates welcome. If you hold open-source data that refines or corrects any parameter in this article, please contact [email protected] citing the specific claim and your source. Verified corrections will be incorporated and credited in the revision history. AI-assisted technical assessment based on open-source material. Not a formal intelligence product.